Quickly and accurately generate your year-end tax documents like W-2 and W-3 reports in CheckMark Payroll. Stay compliant and accurately report employee wages and taxes.

W-2 & W-3 Statements

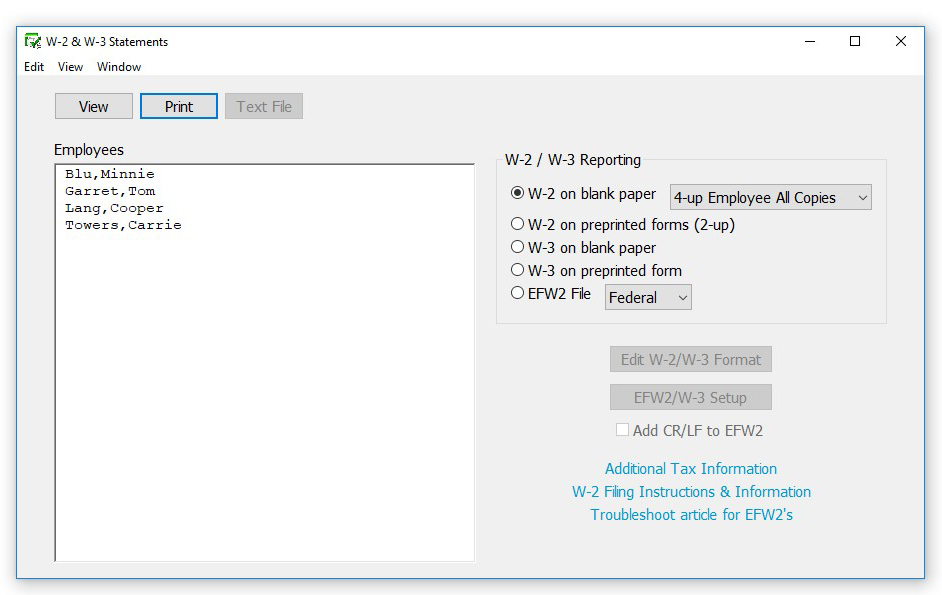

Types of W-2/W-3 Reports

W-2 on Blank Paper Select from this drop-down list, according to the following guidelines:

4-up Employee All Copies – This is for printing employee Copies B, C, and 2 on 4-up blank, perforated paper.

2-up Employer Copy A – This is for printing employer Copy A on 2 plain paper.

2-up Employer Copy 1– This is for printing employer Copy 1 on 2-up blank, perforated paper.

2-up Employer Copy D – This is for printing employer Copy D on 2- up blank, perforated paper.

2-up Employee Copy B– This is for printing employee Copy B on 2- up blank, perforated paper.

2-up Employee Copy C – This is for printing employee Copy C on 2- up blank, perforated paper.

2-up Employee Copy 2 – This is for printing employee Copy 2 on 2-up blank, perforated paper.

| W-2 on Preprinted Forms | This is for printing employee and employer W-2s on preprinted W-2s. |

| W-3 on Plain Paper | Select this option for printing on a W-3 form on plain paper (minimum 20 lb. weight). |

| W-3 on Preprinted Form | Select this option if you are printing on a preprinted W-3. |

| EFW2 File | Select this option if you are required to file electronically with the Social Security Administration or your state. |

Note: Not all states are supported using the EFW2 method.

Creating W-2 and W-3 Reports

The W2 & W3 Statements window allows you to print W-2 and W-3 information on blank perforated sheets or pre-printed forms. You can also save your W-2/W-3 information in the EFW2 file format for electronic filing.

Withholding for Two States

CheckMark Payroll will print State wages and State withholding for up to two states as long as you have not started mid-year or edited YTD totals on Employee Setup. If an employee has income in two states, at least one state needs to have at least $0.01 withheld for the program to recognize both states. If you have withheld for more than two states, you need to prepare multiple W-2s. This can be accomplished by setting up a new employee for each state requiring wages and withholding.

Verify Company Information

Before printing W-2s, you should verify your company name, address and Federal ID are correctly entered on the Company Information window. Your State ID can be verified by selecting State Taxes under the Setup menu. Select each state table from the State Taxes section and verify the State ID.

Dependent Care Benefits – Box 10

If you have a dependent care assistance program (section 129 or section 125 cafeteria plan), the expenses paid or fair market value of those services should be shown in Box 10. Check the applicable box in Additional Income or Deduction setup.

Non-Qualified Plans – Box 11

This box shows distributions to an employee from a non-qualified plan, or deferrals under a non-qualified plan, that became taxable for social security or Medicare taxes during the year, but were for services in a prior year. Check this box under the Additional Income set up screen. Also in the Additional Income set up, mark the check box if plan is a Section 457(b) plan.

Deductions Appearing in W-2 Boxes 12a -12d

Certain deductions should be listed in Box 12 with their appropriate letter code. Refer to the IRS publication Instructions for Form W-2 for a reference guide of Box 12 Codes.

The code “D” that is associated with the 401(k) contribution does not have any bearing on the position in box 12 that the information prints. From the IRS W-2/W-3 instructions: “Box 12-Codes. Complete and code this box. Note that the codes do not relate to where they should be entered for boxes 12a-12d on Form W-2.”

If you wish more explanation regarding printing of your W-2 information, there is a copy of the W-2/W-3 instructions in .pdf format located in the IRS forms folder inside the Payroll folder on the hard drive of your computer, or you can download a copy from the IRS website at www.irs.gov.

Box 13 Check Boxes

On the Employee Setup window, under the Taxes tab, check the box Statutory Employee for employees whose earnings are subject to social security and Medicare taxes but not subject to Federal income tax withholding. There are workers who are independent contractors under the common-law rules but are treated by statute as employees. These are called statutory employees. See Pub. 15-A for details.

Check the box Retirement plan if the employee was an “active participant” (for any part of the year) in any of the following retirement or annuity plans: 401(a), 401(k), 403(a), 403(b), 408(k) (SEP), 408(p) (SIMPLE), 501(c)(18), or a plan for Federal, state, or local government employees. Do not check this box for contributions made to a nonqualified or section 457(b) plan.

Check the box Sick Pay if any employee received sick pay benefits during the year from a third party.

Box 14 – Other

Box 14 can be used for information (Income or Deduction items) that you wish to identify for your employees. Examples include state disability insurance taxes withheld, union dues, uniform payments, health insurance premiums deducted, non taxable income, educational assistance payments, or a clergy’s parsonage allowance and utilities. Check the Box 14 W-2 Options in the Setup window for the Additional Income or Deduction you wish to report.

On the W-3 in Box 14, employers that had employees with Federal withholding by a third party payer will show amount withheld on sick pay of all employees this applies to. This amount is also included as part of the total in box 2 for the W-3. This amount must be reported in both places.

Box 15

Box 15 shows State/State ID#. If you withhold in more than one state, there will be an ‘X’ showing in this box and no state ID entered.

An ‘X’ will appear on the W-3 in box 15 if you withhold for more than one state in a single payroll company.

Furnishing Copies B, C, and 2 to Employees

Furnish copies B, C, and 2 of Form W-2 to your employees, generally, by January 31st. You will meet the “furnish” requirement if the form is properly addressed and mailed on or before the due date.

If employment ends before December 31st, you may furnish copies to the employee at any time after employment ends, but no later than January 31st. If an employee asks for Form W-2, give him or her the completed copies within 30 days of the request or within 30 days of the final wage payment, whichever is later. If you terminate a business or are unable to furnish W-2s by the due date, see the IRS Instructions for Forms W-2 and W-3.